I have, to my surprise, suddenly retired.

This has various ramifications, mostly pleasant ones, but among which is that I need to retool my tax resistance strategy. That strategy has until now involved avoiding or resisting taxation on earned income by means of things like tax-deferred retirement contributions. Now I have to prepare for a future without any earned income to speak of, in which I will instead be drawing down those tax-deferred accounts.

This is my first draft of a game plan for the coming years. There are a lot of moving parts and a lot of uncertainty, and so it’s been challenging to draw this up.

I decided not to adjust numbers for inflation. I figure that allowable HSA deductions, standard deductions, Social Security, etc. will more or less track inflation and so it will be a wash as far as my calculations are concerned. I also assume a 3% real rate of return on invested money, which I understand is considered to be on the conservative end of what is likely (but who knows?).

The further my plans go into the future the more unreliable they are because of all of the unknowns (what will the market do? what will Congress do about Social Security? will artificial intelligence turn us all into paperclips?). For want of a way to meaningfully plan for possible scenarios like the collapse of the U.S. government, the global dominance of artificial superintelligence, and so forth, my scenarios instead assume that the future will be more or less a later-to-arrive version of the present, in which I am older but playing essentially the same game by the same rules. I’m posting this here today in part so I can look back at it and laugh later.

The biggest unknown, or one that looms large in my mind anyway, is how long I’ll be around to enjoy retirement. One can’t count on even one more day, but one ought to plan ahead anyway. The typical life expectancy for someone my age is something like 81. But my parents are both alive and on the cusp of 90 and three of my four grandparents made it into their 90s too, so I think I should be prepared for the possibility that I may stick around longer.

My goal is to have a comfortable and secure retirement (and hopefully a long and healthy one) and to continue to successfully resist funding the U.S. government. Can I do that if I retire today?

Just about every year since I started resisting, I’ve put aside 40–50% of my income into tax-deferred retirement accounts and a health savings account (HSA). In years when my income was lower than it needed to be to avoid the federal income tax, I’ve transferred some of the tax-deferred money into a Roth IRA, taking that amount as current-year income while staying within the 0% tax bracket. A couple of years back I stopped using the HSA to pay for health expenses and started using it as another retirement savings vehicle.

Early Retirement: Ages 57½–59½

So I start with a pretty good hunk of change in retirement accounts. However, I’m only 57½. I cannot begin to tap these accounts without penalty until I turn 59½, with a couple of exceptions:

- I can withdraw from my HSA to pay for past health expenses I had paid for out-of-pocket (yes, I saved the receipts), and for current health expenses.

- I can withdraw from my Roth IRA any principal I added at least five years ago (but not any gains, or anything I added more recently).

So for the next two years, before I turn 59½, I need to live off of my current cash savings (~$24k) + about $2k from my HSA + about $38k from my Roth = $64k. Can I do that?

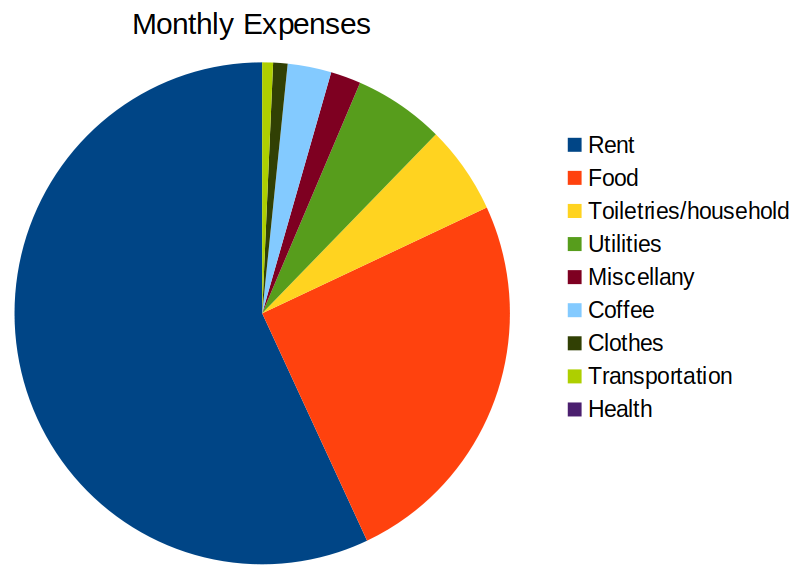

My current spending runs to about $27k per year in rent, food, etc. (not counting health expenses for which I could tap the HSA). $64k gives me twice that and then some, so that feels safe to last two years.

I have brought in only about $15k in earned income this year. But I was making HSA and IRA deposits as though I were going to earn a standard year’s income. As a result I have way more deductions than I need to shield that much income from income tax. This gives me the opportunity to generate more tax-free income by doing another Roth transfer this year, probably to the tune of $43k or so. That will help later on.

Pre-Medicare: Ages 59½–65

When I turn 59½ I can start drawing down both my tax-deferred and Roth IRAs as much or as little as I’d like. (Starting at age 75, required minimum distributions may change this calculus a bit; I’ll get to that later.)

If I pull no more than $22k from my tax-deferred IRA per year, and deposit the maximum (currently $5,400) in my HSA, this will result in an adjusted gross income less than the standard deduction, resulting in no taxable income. (This also ensures that I remain eligible for Covered California’s high-deductible health insurance plan, so I can make HSA deposits.) Because none of this income is considered earned income in the current tax year; there is also zero self-employment / social security tax. If I supplement that ~$16k spending money with another $21k from my Roth IRA, that gives about $37k in spending money.

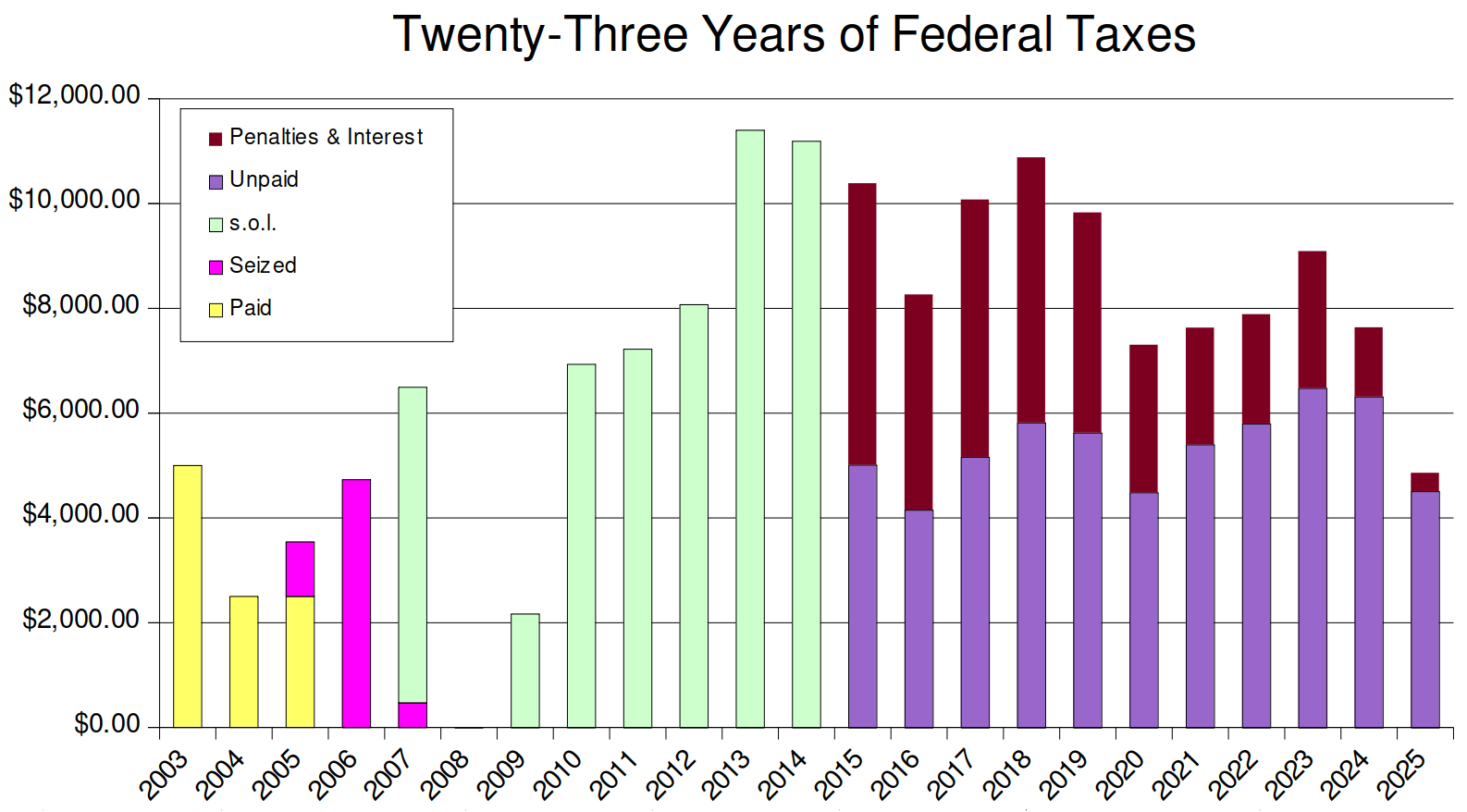

For the next several years I hope that the IRS will continue to drop the ball on my past tax debt, letting it fall off the statute of limitations cliff year after year as they have for several years now. When they do this, I typically celebrate by making a charitable donation equal to the amount of the successfully resisted taxes. I hope to keep doing this, but this means subtracting $4–$6k from that $37k of spending money. But that still leaves me comfortably above my $27k budget, so I think I’m okay here.

Medicare Kicks In: Ages 65–69

When I have to join Medicare at age 65, I lose my high-deductible health insurance plan and can no longer contribute to my HSA. Medicare also has substantially more expensive premiums than my current plan. As a result, my healthcare expenses rise, and an important tax deduction vanishes.

This will be a good time to start tapping my HSA to pay for these extra expenses.

On the up side, my standard deduction increases to the You’re Officially Old level.

In 2037, if things go well, the last of my tax debts will be eliminated by the statute of limitations. I’ll make my usual charitable donation and will have no remaining federal tax debt.

Things are a little iffy toward the end of this 65–69 range: it’ll be touch-and-go depending on the market and on how frugal I’ve been in the previous years, but I may exhaust my Roth toward the end of this period. If so, I have options. I might tap the HSA to reimburse for past medical expenses (if I still have any stored up), or I might have to take more out of my tax-deferred IRA, which could put me into taxable income territory. Another option would be to apply for Social Security earlier than I otherwise planned to.

What if the IRS Seizes that Tax Debt?

The IRS has failed, for many years running, to collect taxes they say I owe them. But this isn’t because I have some great ninja asset-hiding scheme. I haven’t buried my IRA in a hole in a tax haven or anything like that. I’ve just been overlooked by a dysfunctional bureaucracy. That could change at any time.

The total amount I owe at this point is a little under $90k. If the IRS seizes money from some account of mine, that may have additional tax implications. If they seize it from a tax-deferred retirement account or from my HSA, the amount they seize would count as potentially-taxable income in the year it was seized. (I think early-withdrawal penalties are waived in such a circumstance, but if not, that too might be an issue if this happens before I turn 59½.) If they seize it from my bank account or from my Roth, that leaves less in those accounts for me to use to offset potentially-taxable income.

In short, such a seizure could throw a wrench in my plans, and I’d have to rejigger things.

Because it’s difficult to predict if, when, or in what manner this might happen, I haven’t tried to account for this in my scenarios. But it’s a Sword of Damocles that dangles over these plans and could disrupt them a bit.

One thing I’m unsure about is whether the act of beginning to draw down my retirement accounts will make those accounts more salient to IRS enforcers. I think they tend to be reluctant to seize money from retirement accounts; but this may be more the case when those accounts represent retirement savings than when they represent retirement income. It’s possible that beginning to take IRA withdrawals may trigger a levy.

Of the ~$90k in tax debt, about a third of it is interest and penalties added by the IRS to the amount I originally did not pay. If seized from me, I could apply to the War Tax Resisters Penalty Fund for reimbursement of these penalty-and-interest amounts. The fund has a good record of reimbursing requests like these, but it has not seen many requests in recent years, and a request for ~$30k would be an especially large one, so it is uncertain how much reimbursement I could expect from such an application. I am not sure whether such a reimbursement would officially be considered taxable income or more along the lines of a gift.

Social Security Kicks In: Ages 70–74

When I hit age 70, I must begin taking Social Security (I could start earlier, but I think it is to my advantage to wait). In current dollars, my expected benefit is about $35k/year. (The Social Security trust fund is expected to give out by then, which could mean a reduction in benefits if Congress has the guts to try that. This would change some of the numbers that follow, but not the basic strategy.) Social Security benefits are taxable, but only according to a strange formula:

- If your “combined income” is < $25k, they aren’t taxed at all.

- If your “combined income” is between $25k and $34k, half of your Social Security benefits become part of your adjusted gross income.

- If your “combined income” is > $34k, 85% of your Social Security benefits become part of your adjusted gross income.

So my best bet for avoiding federal income tax entirely is to keep my “combined income” below $25k. What is “combined income” you ask? It seems to be whatever would be my adjusted gross income anyway (at this point: what I pull from my tax-deferred IRA, plus any Roth conversions) plus half of my Social Security benefits.

Naïvely, if I were to continue to withdraw about $20k/year from my IRA, my “combined income” would be about $38k, which is too much. So what can I do about that?

There’s a trick called “qualified charitable distributions” that allows retirees after age 70 to transfer money directly from their tax-deferred retirement accounts to certain types of charities; when they do so the amount of the transfer does not count as income. So if I get $35k in Social Security, withdraw $7k from my IRA to supplement that, and donate $13k to charity from my IRA, the numbers look something like this:

- Spending money: $35k + $7k = $42k

- Combined income: $35k÷2 + $7k = $24.5k

- Adjusted gross income: $7k

So I remain tax-free despite the new income source, and indeed my spending money budget can go up. If I stay frugal, I can even use some of this extra money to rebuild my Roth by means of Roth conversions. That may come in handy later on when my HSA runs out (around age 77 according to my projections).

Social Security can be seized by the IRS to satisfy tax debt. (Typically only 15% of your check can be seized, but more can if The Man decides to make a big deal about it.) However if things go well I won’t have any remaining tax debt by the time I turn 70, so this won’t be an issue.

You may wonder why I plan to withdraw anything at all from my IRA at this point, since the Social Security benefit by itself wouldn’t be taxable and yet would be enough for me to live on comfortably. The answer is that I have to withdraw some of that money eventually — see below — and so there’s no real disadvantage to doing so at this stage if there’s plenty to be had. If I don’t have any spending needs to justify the withdrawals, I can take them in the form of Roth conversions and charitable contributions. If the market tanks, I can leave my IRA alone and coast on Social Security for a while.

Required Minimum Distributions: Ages 75+

At age 75, another rule kicks in: I must take a certain amount from my tax-deferred IRA every year whether I want to or not (up to now, whether and how much to withdraw has been entirely up to me). The amount I have to withdraw is based on the amount in the account and my age. Under the projections I’m working with, this will have the effect of slightly increasing the amount I withdraw from my IRA.

But because of the “qualified charitable distributions” trick described above, I can simply increase my charitable giving to match and thereby continue to keep my combined income and adjusted gross income numbers below their respective lines.

I’ve run the numbers through 2068 at which time, if I am still alive and kicking, I will celebrate my 100th birthday. Should I be so lucky, according to my best-guess estimates, I will have spent about $2.3 million in today’s money on my own modest upkeep during retirement, will have given about $600k to charity, and will still have a little gas in the IRA tank in case they’ve invented a miracle longevity pill or I want to leave a bequest somewhere or other. When I look at it that way, I feel astonishingly wealthy and fortunate (though fortune may have its own ideas for my future). Yet, when I describe my frugal retirement strategy to others I not infrequently am met with a response that suggests I’m consigning myself to sad poverty or something like that.

What if I have unusual expenses I haven’t anticipated here, e.g. I need long-term care or I want to take a bucket list vacation somewhere fancy or I want to replace my failing body with the latest consumer model robot parts? Well, I do have a considerable extra room in my potential budget if I’m willing to step over the taxable income line. If in some year I need to spend thousands of dollars on some emergency (or splurge) expense, I can withdraw a little extra from the IRA or I can neglect to make a charitable donation that year. This makes me vulnerable to income tax, but I can always just neglect to pay the tax and try my luck against the IRS enforcement bureaucracy, which has been a good bet thusfar.

Of course, nothing will turn out exactly like I’ve planned. Trying to project things 40 years into the future based on the current financial economy and political economy and my current lifestyle needs is nuts. But as a back-of-the-envelope calculation to help me figure out whether now is a good time to attempt to slip into a secure retirement and continue to resist, it’s been a good exercise and has given me the confidence to go ahead. It’s also helped me to plot out some strategies I can use along the way (if I stay alert for changes and remain flexible) to make things go easier.

| ages | 0-tax target | strategy |

|---|---|---|

| 57½–59½ | AGI < $16,100 | Limited Liquidity: Spend down cash, use Roth principal to supplement. Continue maximum deposit to HSA. Do Roth conversions to fill out your 0% bracket. Pay medical expenses without dipping into the HSA. Continue ~$5k/year charitable contributions. Your post-medical spending budget is ~$30k/year. |

| 59½–65 | AGI < $16,100 | IRAs available: Tap tax-deferred IRA to the extent you can while remaining in the 0% bracket (~$22k). Otherwise pull from the Roth. Only do Roth transfers if you have extra room in your 0% bracket. Continue maximum deposit to HSA. Pay medical expenses without dipping into the HSA. Continue ~$5k/year charitable contributions. Your post-medical spending budget is ~$30k/year. |

| 65–69 | AGI < $19,050 | Medicare: You must join Medicare, so you lose the health insurance plan that allows HSA contributions. Your standard deduction rises, so you can pull more (~$25k) from your IRA. Pull whatever else you need from the Roth. Medical expenses likely to rise (Medicare premiums and deductibles); budget about $6.5k for this, but pay from your HSA. Continue to make charitable donations until the last tax debt vanishes in 2037. Your post-medical spending budget is ~$30k/year. |

| 70–74 | CI < $25,000 | Social Security: Your Roth may be depleted; you may have to rely on your tax-deferred IRA. You begin taking Social Security, about $35k per year. Make “qualified charitable donations” directly from your tax-deferred IRA to keep your combined income low. Make more Roth conversions if you can, as this will come in handy when your HSA gives out. Your post-medical spending budget is ~$40k/year. |

| 75+ | CI < $25,000 | Required Minimum Distributions: Your Roth may be depleted, and your HSA is emptying as well. This makes it a little more difficult to stay in the zero-tax zone, but still manageable. Increase your qualified charitable donations to make up for additional IRA withdrawals. Your post-medical spending budget is ~$35–40k/year. |